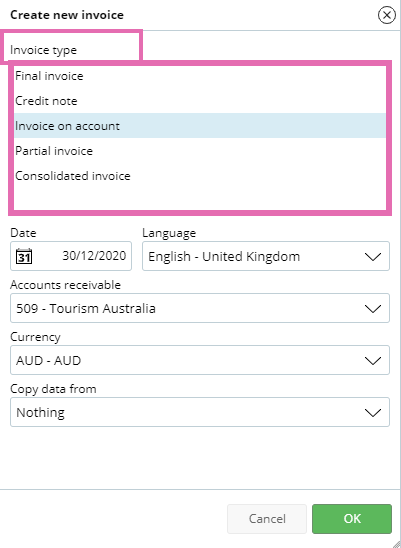

A partial invoice is most commonly used when invoicing time and expenditures on jobs. In order to create a partial invoice, job expenditures need to be financially posted first. Often financial teams will be involved in partial invoicing, as this invoice type is usually configured to recognize revenue via the invoice. Once a partial invoice is posted, billings are posted straight to the profit and loss, reducing work in progress (WIP) accounts.